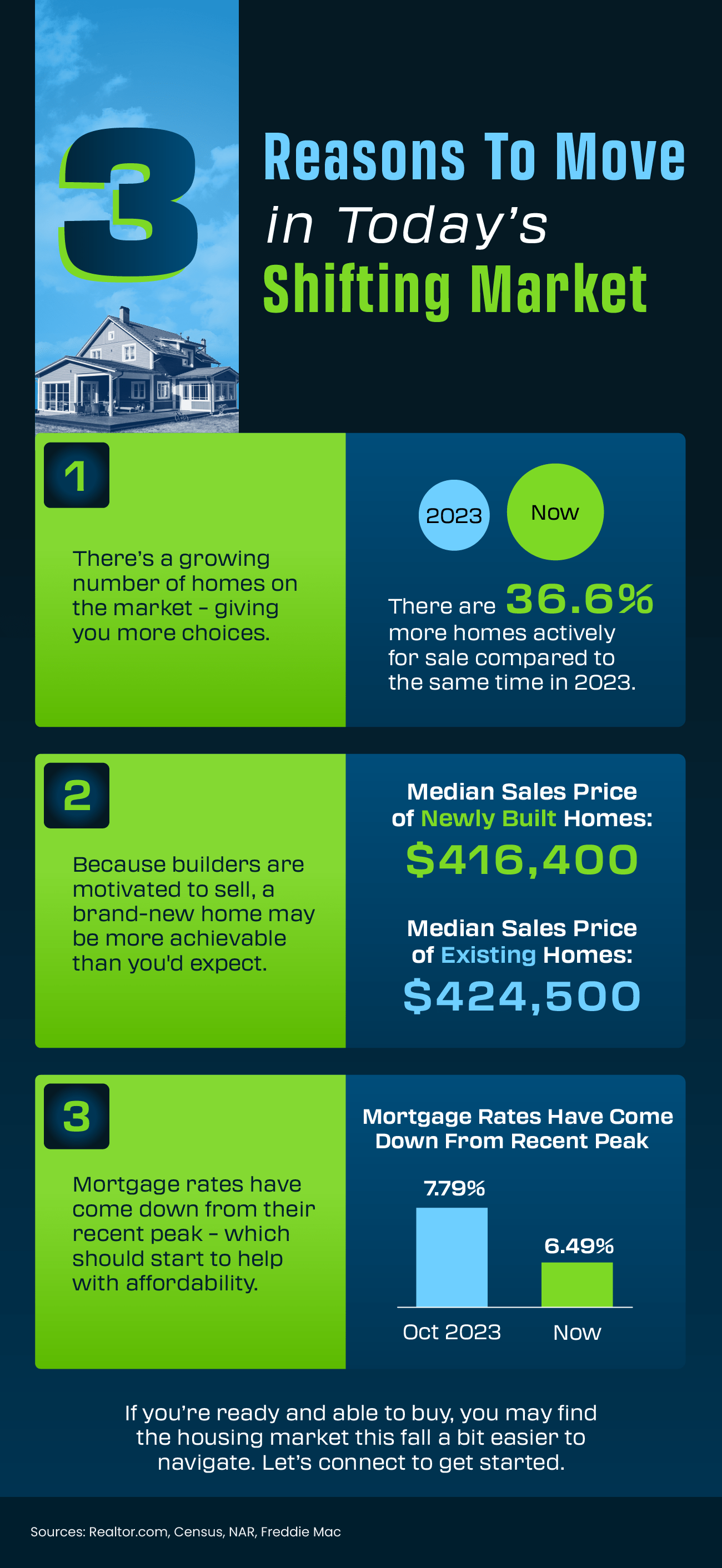

Some Highlights

- The housing market is in a transition. And that gives you 3 key opportunities going into the fall.

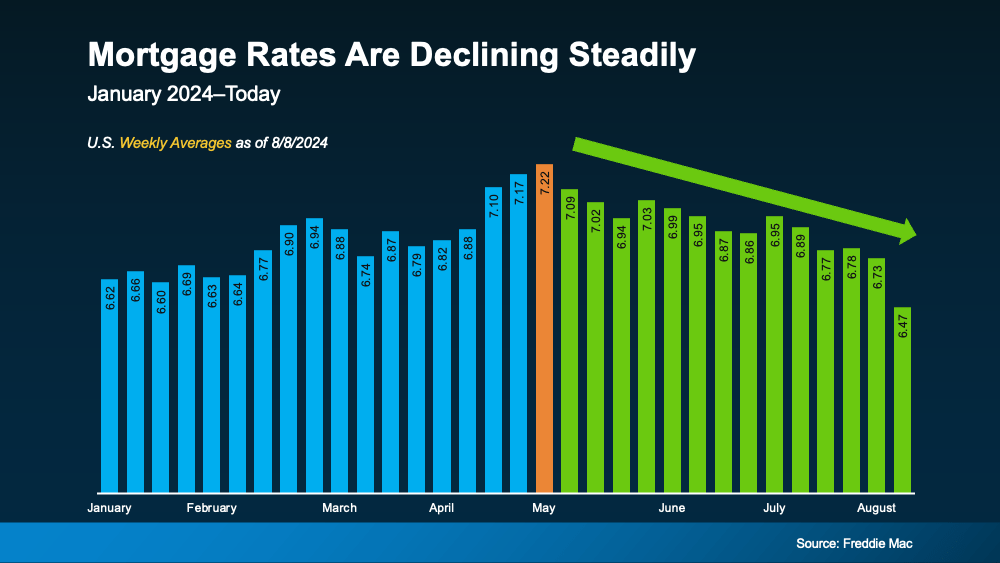

- There are more homes actively for sale. Builders are motivated to sell, so a newly built home may be more achievable than you think. And mortgage rates have come down from their recent peak.

- If you’re ready and able to buy, you may find the housing market this fall a bit easier to navigate. Connect with an agent to get started.

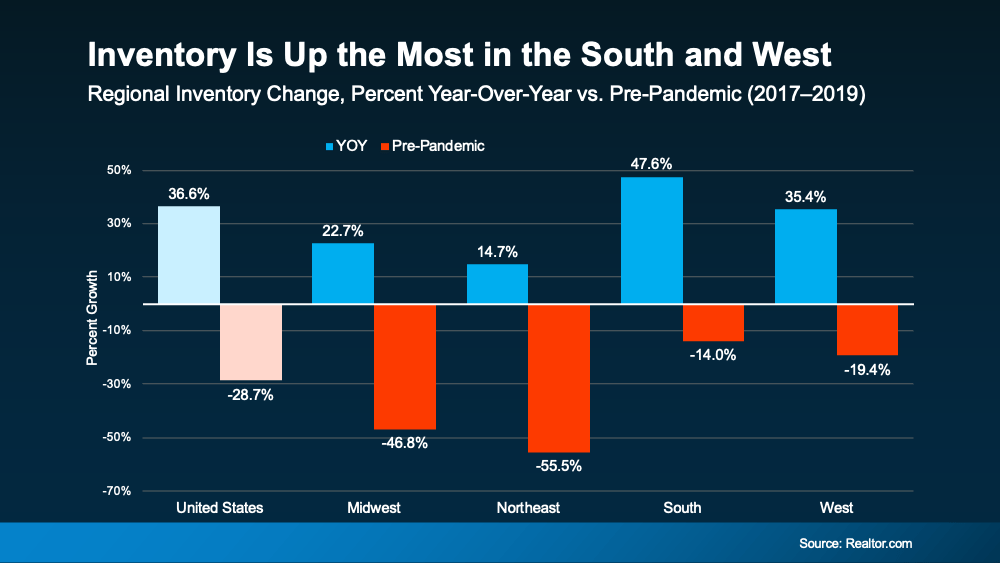

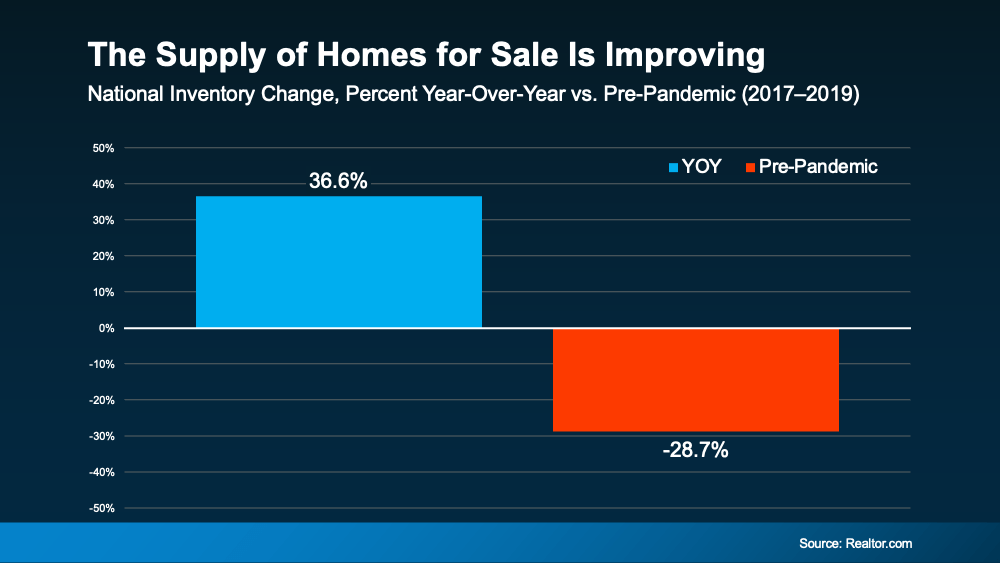

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.