Some Highlights

- There’s a misconception Wall Street is buying all the homes on the market. But data proves that isn’t true.

- Experts agree the share of homes bought by investors is declining – and most are smaller investors, like your neighbor who owns a second home, not Wall Street.

- No matter what you’ve heard, the majority of homes are still being purchased by everyday homebuyers like you – not big investors. Connect with an agent if you have questions.

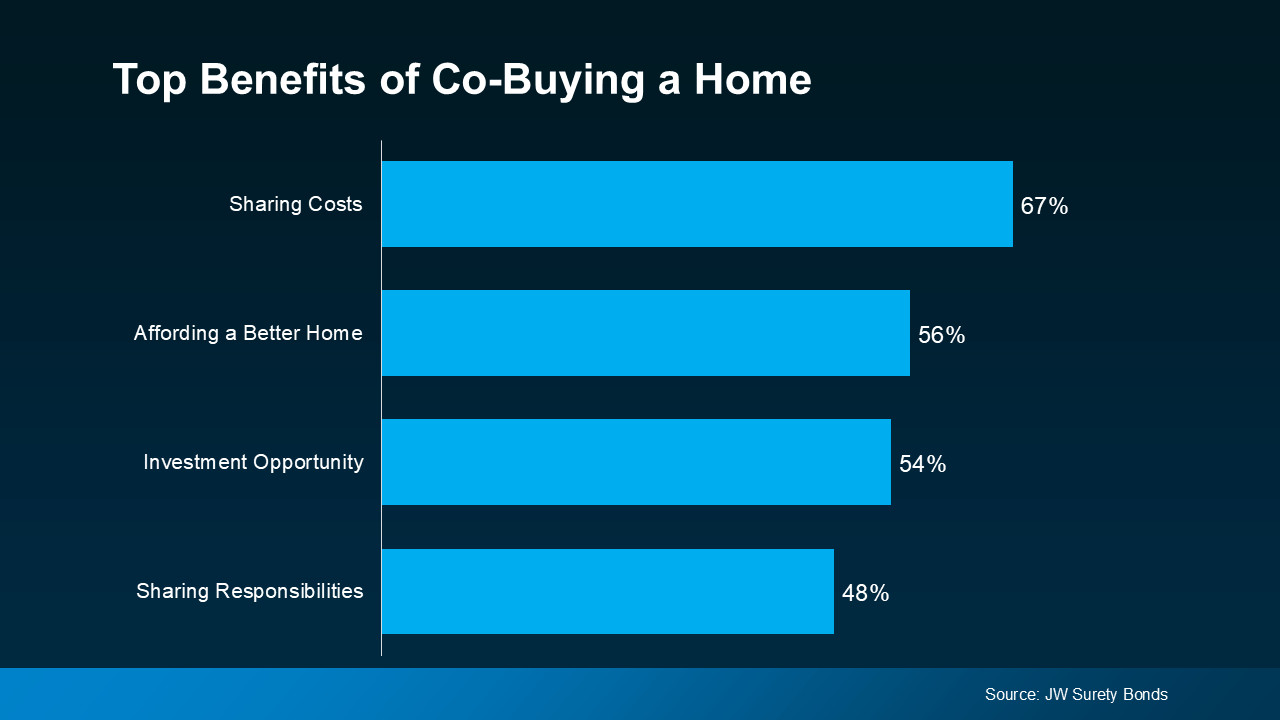

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.