Spend about 5 minutes online searching for news about the housing market, and odds are you’ll see something pop up about home prices. You may even stumble onto social media influencers saying we’re headed for a crash. Let’s get you the context you need.

The truth is prices are going to vary depending on where you live. But they’re not crashing.

Here’s what you need to know.

The Local Perspective: Home Price Trends by Area

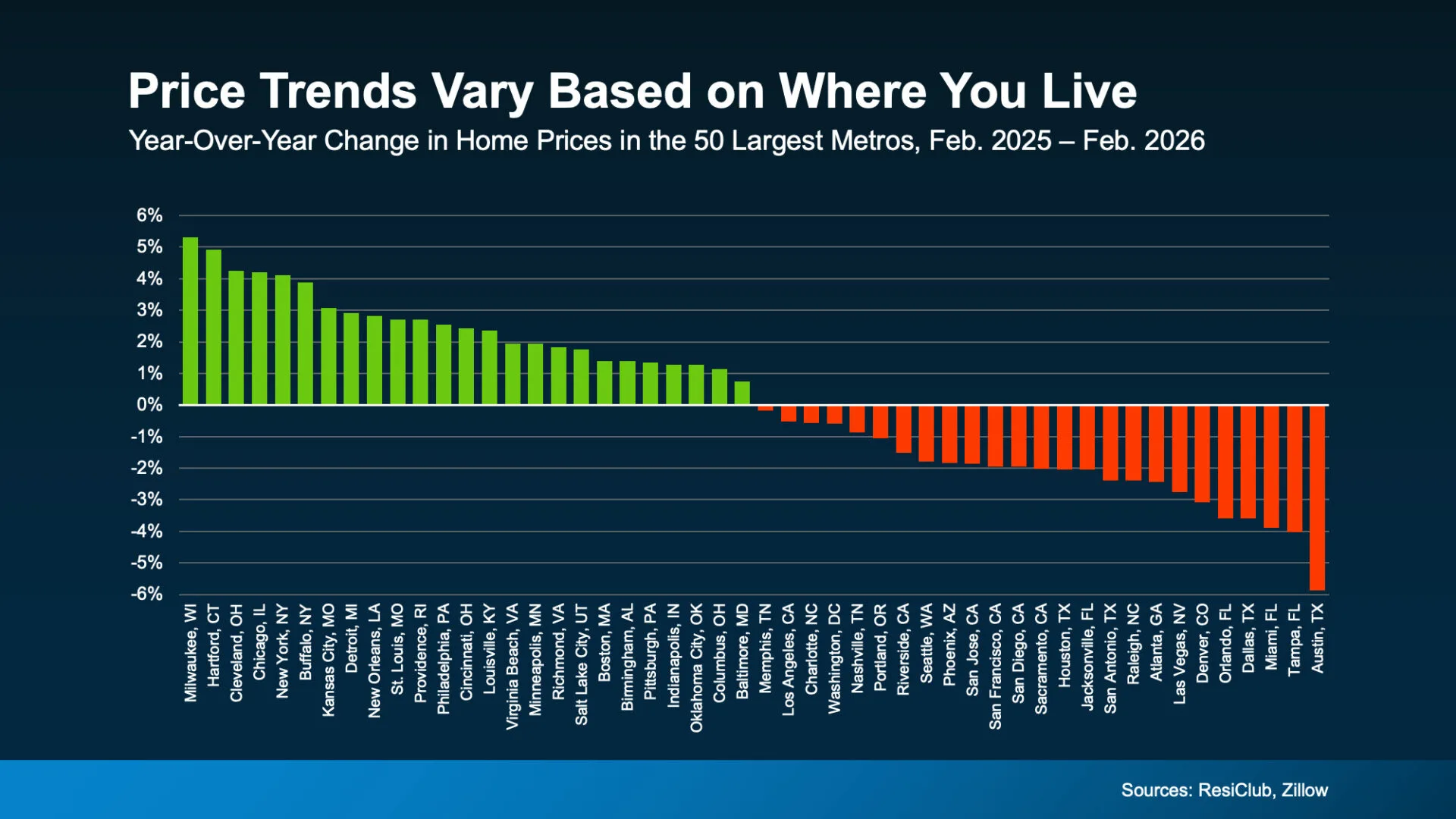

The biggest thing feeding into the confusion online is how different home price trends are by area right now. Take a look at this data from ResiClub and Zillow (see graph below).

About half of the largest metros are seeing prices go up.

The other half are seeing some declines.

Unfortunately, the online chatter only focuses on the markets where prices are down – and that makes it sound like something bigger is happening.

Unfortunately, the online chatter only focuses on the markets where prices are down – and that makes it sound like something bigger is happening.

But, as you can see in this graph, that’s only one side of the story. The full picture is different.

The National Perspective: Moderate Price Growth

As a country, when you average it all together to get a true baseline, one thing becomes clear, home prices are still net positive at the national level.

According to the Redfin, national home prices were up about 1% year-over-year in February. So, what we’re seeing right now isn’t a collapse. It’s a market that’s normalizing after a period of unusually fast growth. And that impacts some local markets more than others – particularly those where prices rose too far, too fast during the pandemic.

A true crash, like what happened in 2008, would mean prices dropping sharply across the entire country. That’s just not what the data shows today. And it’s not where things are going either.

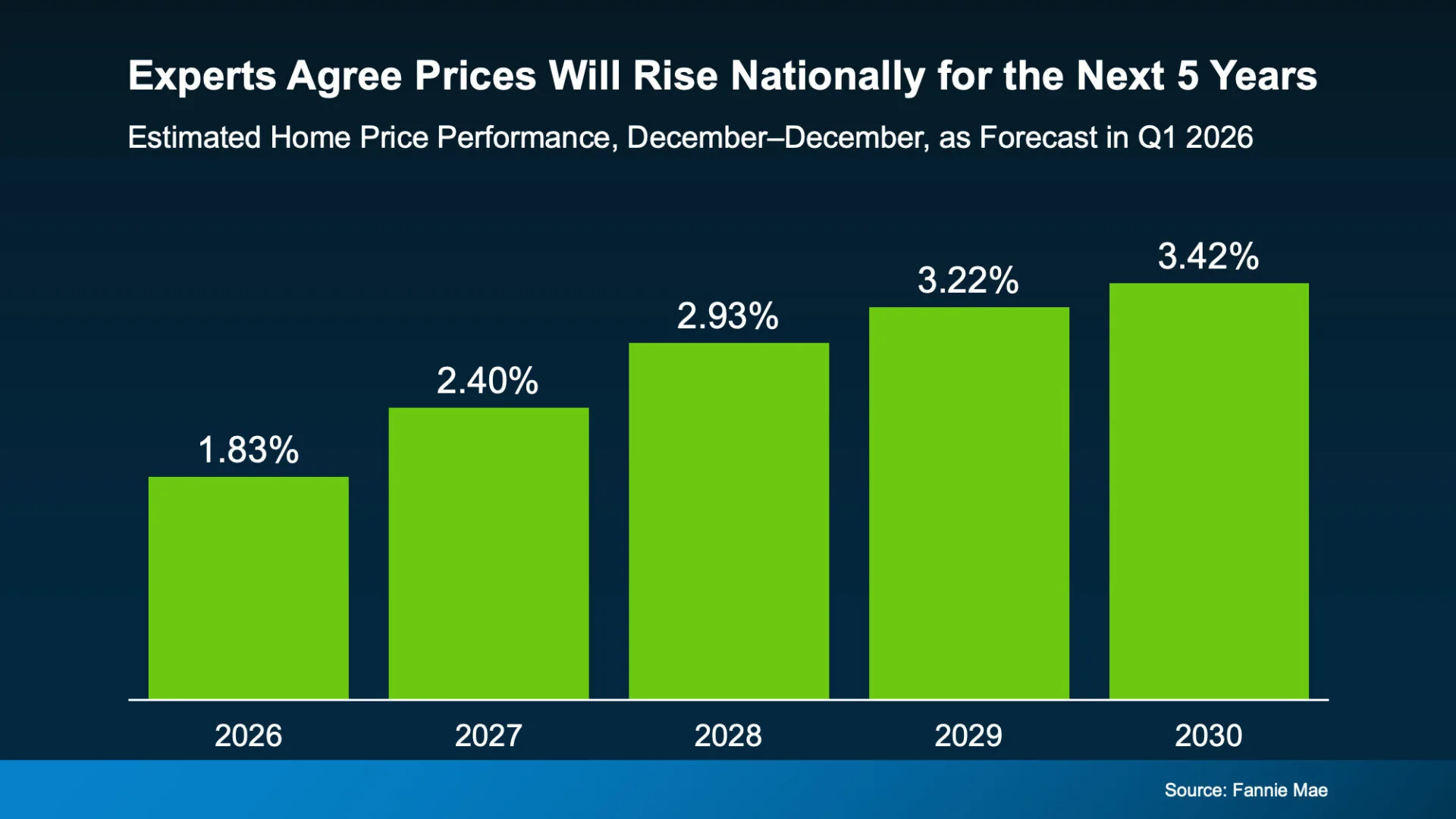

Experts Agree This Isn’t 2008

In fact, Fannie Mae surveyed over 100 housing market experts to ask their opinions on where prices are headed from here. And the experts agree, nationally, prices are expected to keep rising over the next five years:

That rise will be moderate, particularly this year, but the trend is clear. Nationally, prices are forecast to grow every year now through at least 2030 – and that’s normal. Daryl Fairweather, Chief Economist, at Redfin explains:

That rise will be moderate, particularly this year, but the trend is clear. Nationally, prices are forecast to grow every year now through at least 2030 – and that’s normal. Daryl Fairweather, Chief Economist, at Redfin explains:

“House prices aren’t going to fall on a national scale any time soon—and that’s actually a good thing. It’s normal for house prices to rise gradually over time . . .”

That’s why even in the select areas where prices have dropped slightly this year, the decline is expected to be temporary. According to that same quarterly Fannie Mae survey mentioned above, 85% of the experts say the markets that are seeing mild declines right now will return to positive price growth before the end of 2027.

The main takeaway? This isn’t a crash. And prices aren’t expected to fall nationally. If anything, the few areas experiencing declines are expected to rebound in the next year or so.

Bottom Line

It’s easy to get caught up in headlines that make it sound like something big is about to happen. But don’t be fooled. The housing market isn’t crashing. It’s just shifting.

The key is understanding what’s actually happening in your market, so you can make the right move for you. Connect with a real estate agent if you want the local perspective.